21.08.2019

21.08.2019

VAT Registration – step by step. How to fill in the VAT-R form?

The obligation to register for VAT applies to both natural persons running sole proprietorships and various types of commercial companies. However, the legislator included many exceptions that exempt from paying the goods and services tax. From today’s article, you will find out when it is necessary to register for VAT and how to fill in the VAT-R form.

Is the registration for VAT obligatory?

Registration in the field of goods and services tax, commonly referred to as VAT is required from natural persons, legal persons and organizational units without legal personality, who independently conduct business as producers, traders, farmers and service providers.

The VAT Act contains a number of exceptions that totally or temporarily exempt the entrepreneur from the obligation to account for and pay VAT. These exemptions can be divided into the objective exemption and the subjective one.

The objective VAT exemption applies to entrepreneurs performing only the activities listed in art. 43 sec. of the Act on tax on goods and services.

The subjective exemption concerns, in turn, the sales limit, which in 2019 amounts to PLN 200,000 and in the case of people setting up a company during the year, is determined pro rata, according to the number of months in which the young entrepreneur will operate.

Who has to register for VAT?

You have to register as an active VAT if:

- you deliver products made of precious metals or products with the content of these metals, goods subject to excise duty, excluding electricity and tobacco products, new means of transport as well as construction sites and areas designated for development,

- you provide legal services, consultancy or jewelery services,

- you do not have a registered office in Poland ,

- in the previous year, as part of your business, you exceeded the applicable sales limit.

The subjective exemption does not apply to the entrepreneurs providing services listed in the first three items above.

VAT registration – where to submit documents?

In order to register as active VAT payers, you must fill in and submit the VAT-R application form, which you can download, among others, from the Tax Portal run by the Ministry of Finance. Entries to the VAT register can be made electronically, by post, as well as during a visit to the tax office.

When opting for online VAT registration, you can accomplish that either through the aforementioned Tax Portal – in this case it is necessary to have a qualified electronic signature or a Trusted Profile, and attach the VAT-R application to the application for entry or to change the entry in CEIDG.

How do I fill in the VAT-R form? Step by step instructions

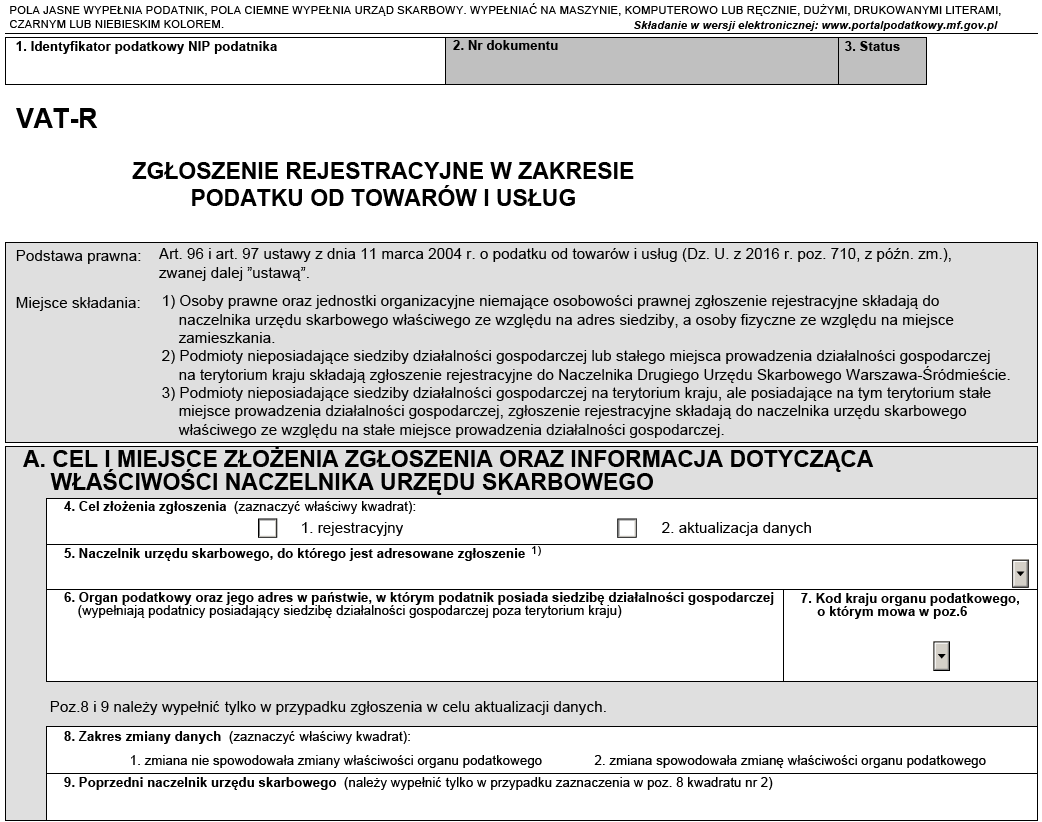

Enter your tax identification number in field 1 (at the very top of VAT-R form), and if you do not have one, attach the identification application NIP-2 to the submitted form.

A. The purpose and place of submitting the application and information on the jurisdiction of the head of the tax office

In field 4, mark the purpose of the application. Then provide information to which the head of the tax office you address the document.

Complete items 6 and 7 only if you have a registered office outside Poland. Items 8 and 9 should be omitted, as they concern data updates.

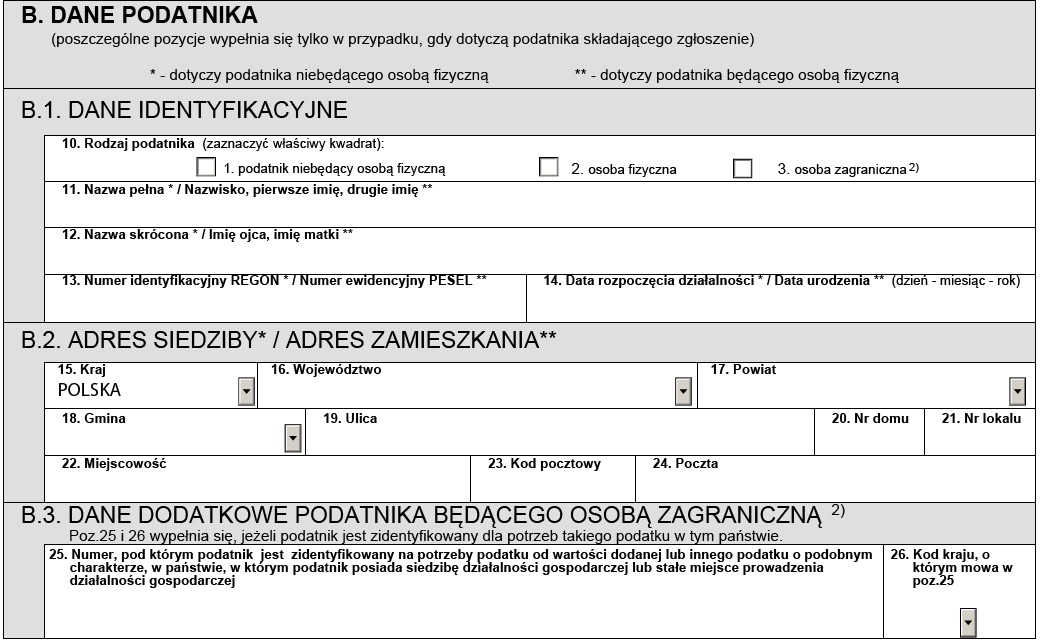

B. Taxpayer’s details

In the subsequent section, provide the most important identification details. You complete individual items only if they concern you. Fields marked with a single asterisk are filled by an entity that is not a natural person; that is legal entities and organizational units without legal personality. Positions marked with two asterisks are filled if you are a natural person; that is, for example, in the case of conducting sole proprietorship.

| Important note! Natural persons, as part of their VAT-R application, use their own name, father’s and mother’s name, PESEL number, date of birth and residence address. Only taxpayers who are not natural persons on the VAT-R form provide the company name, REGON, date of commencement of operations and address of the registered office. |

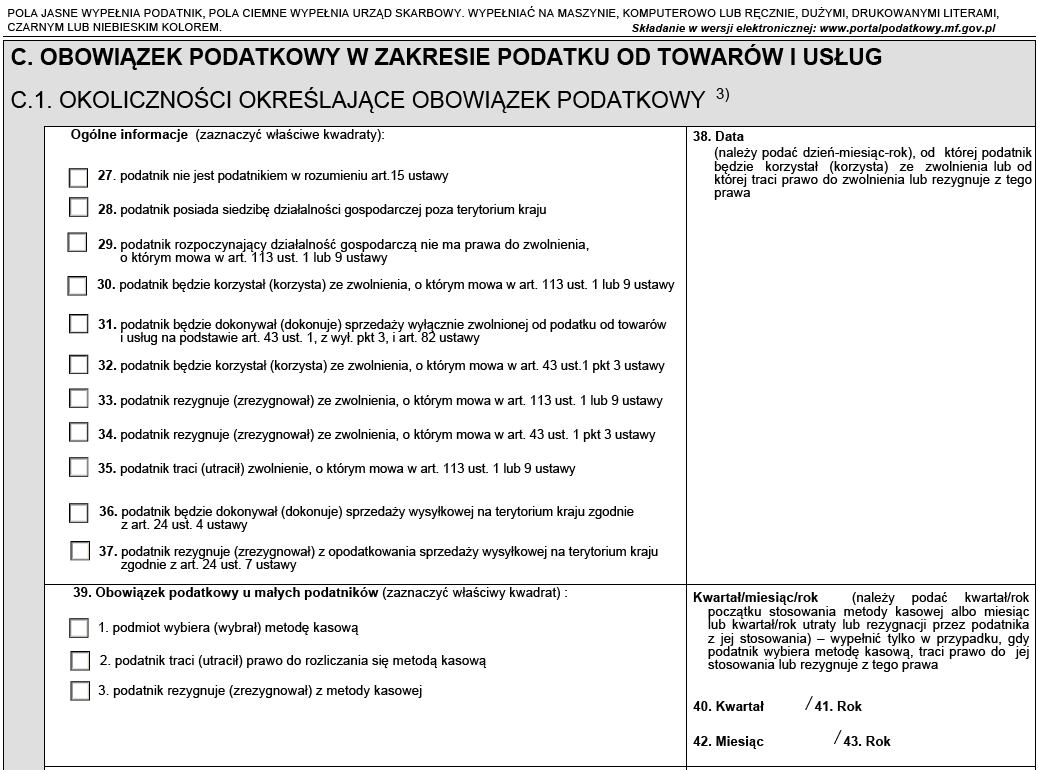

C. Tax obligation in the area of goods and services tax

In section C of the tax form, you must specify the circumstances related to the tax obligation and specify the manner and frequency of submitting VAT returns.

C.1. Circumstances determining the tax obligation

You can skip item 27. Only people who do not run a business mark it.

You mark item 28 only when the registered office of your company is located outside Poland.

You mark item 29 when you do not have the right to subject exemption at the time you start your business. This is the case if, as part of your business, you provide services or carry out the supplies specified in art. 113 par. 13 of the VAT Act (as mentioned above in the paragraph “Who must register for VAT?”).

Item 30 is selected by a person intending to benefit from a subjective exemption, regarding a sales limit of PLN 200,000.

| Important! According to the regulations, you do not need to submit a VAT-R form when you use the subjective exemption. The right is used “by default”. |

You mark item 31 if, as part of your business, you will only perform VAT-exempted sales, pursuant to Art. 43 par. 1, excluding item 3, and art. 82 of the VAT Act.

You mark item 32 when you are subject to the subject exemption listed in art. 43 par. or 9 of the VAT Act.

Item 33 concerns persons who voluntarily forego the subjective exemption, i.e. the exemption resulting from the sales limit. This is the most frequently indicated position by new entrepreneurs who want to enter in the register of active VAT taxpayers.

Mark item 34 if you voluntarily give up the flat-rate exemption for farmers.

Item 35 is selected by entrepreneurs who exceeded the sales limit in the previous year, and thus lost the right to subjective exemption.

Item 36 applies to VAT payers in an EU state outside of Poland who send VAT-taxable goods to Polish companies.

Item 37 can be omitted, as it concerns updating the data from point 36.

In item 38, you must enter the date from which you will be exempt or the date on which you lose your right or resign from the right to exemption.

Item 39 concerns information about the tax liability of small taxpayers. The first field should be marked by the entity wishing to use the right to settle VAT using the cash accounting method (in which the tax obligation arises from the date of settlement of all or part of the receivables). The second field is marked by the entity that lost the status of a small taxpayer due to exceeding the turnover limit. Field number 3 should be selected by taxpayers voluntarily resigning from the cash accounting method.

Items 40, 41, 42 and 43 shall be completed with appropriate dates if you have ticked one of the boxes in box 39.

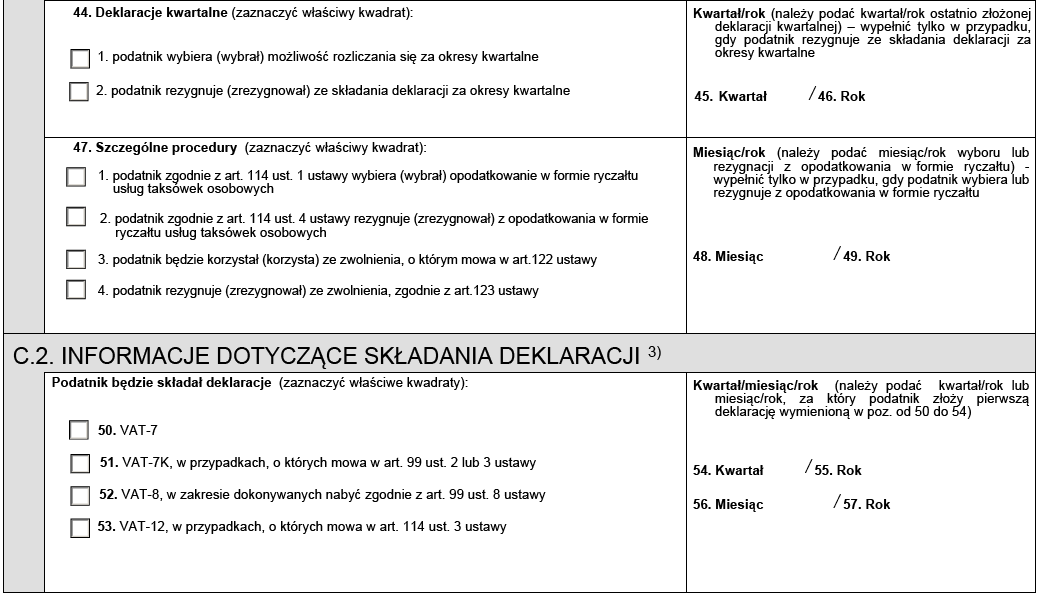

Items 44, 45 and 46 relate to taxpayers choosing or giving up the possibility of paying VAT on a quarterly basis.

Items 47, 48 and 49 shall be filled in if you provide taxi services or supply investment gold.

C.2. Information on the submission of returns

In part C.2 of the VAT-R notification, please provide information on the type of tax returns to be submitted and specify the date of submission of the first document.

- VAT-7 – submitted by taxpayers, who settle on a monthly basis.

- VAT-7K – submitted by entities that are settled on a quarterly basis or taxpayers who settle according to cash accounting principle.

- VAT-8 – this return covers entities obliged to settle intra-Community acquisition of goods.

- VAT-12 – applies to taxpayers providing personal taxi services who chose flat rate taxation.

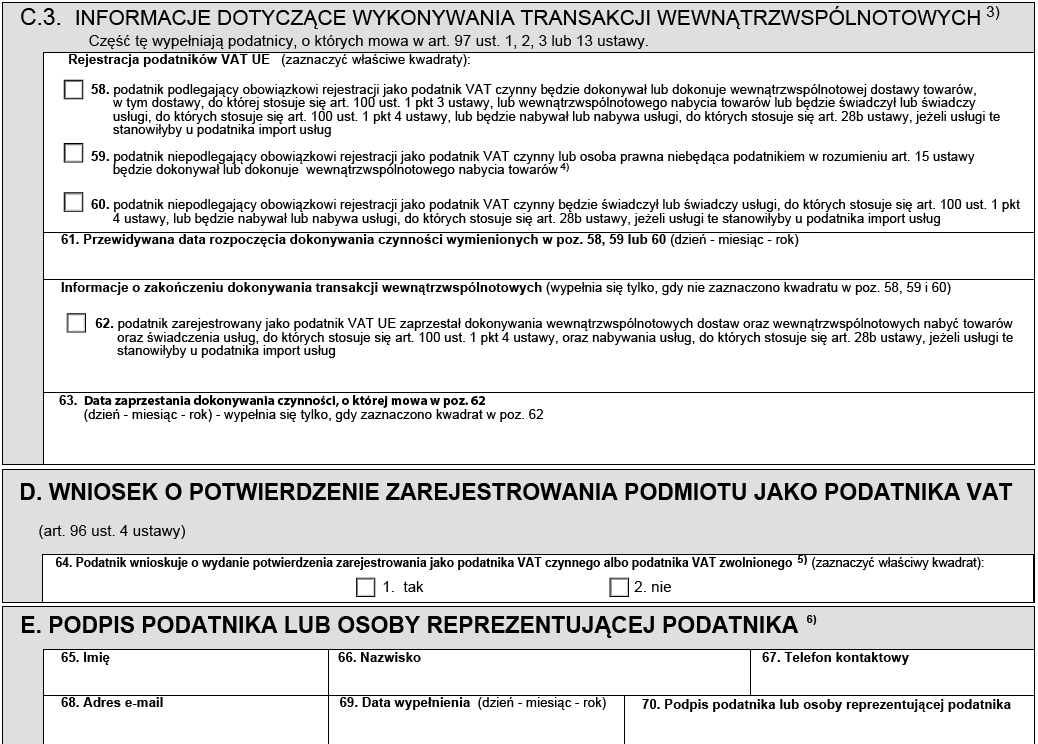

C.3. Information on the execution of intra-Community transactions

Section C.3 of VAT-R shall be filled in by entities wishing to register as EU VAT taxpayers. In the following items (from 58 to 63), you must provide circumstances specifying the tax obligation, as well as the start and end dates of your intra-Community transactions.

By filling in section D of the VAT-R form and paying the appropriate fee, you will receive a confirmation of registration of the entity as an active VAT payer. This is not an obligatory part of the VAT-R declaration.

The VAT-R declaration is made for the purpose of registering or updating VAT data. The entry in the VAT register is free of charge and the application can be made electronically.